2024-02-02

This post will be about valuing private companies. It will explore the differences between private and public companies, weigh the associated pros and cons, the valuation process, and build a small case study. Expect a comprehensive discussion that may extend the post's length.

Typically, when valuing companies, the focus is on public entities – well-established, often larger enterprises. In these cases, revenue and earnings are generally more stable compared to smaller private counterparts. An additional divergence lies in accessibility; for public companies, one can easily retrieve financial information by visiting their investor relations page or searching on platforms like sec.gov. Conversely, for private companies, acquiring financial data may require direct contact or reliance on platforms such as North Data or Bundesanzeiger, particularly in the context of Germany.

Other differences arise in how one approaches the valuation process. Typically, when valuing companies, the common standard is Discounted Cash Flow (DCF) analysis. However, this approach may not be suitable for private companies. Projecting cash flows for ten years and determining a fair discount rate can be challenging and uncertain.

Instead, an Asset-Based approach can be employed for private companies. This involves valuing the business based on its assets, utilizing metrics such as book value, Fair Market Value (FVM), or Liquidation Value (LV). While the DCF method is less prevalent due to uncertainties, the most frequently used approach is the Multiple Approach.

To understand the Multiple Approach we will go through each variable of the formula.

Various benchmarks can be utilized for valuing a company. Below are some listed, along with the scenarios in which they are commonly applied:

How to calculate Adjusted EBITDA Example

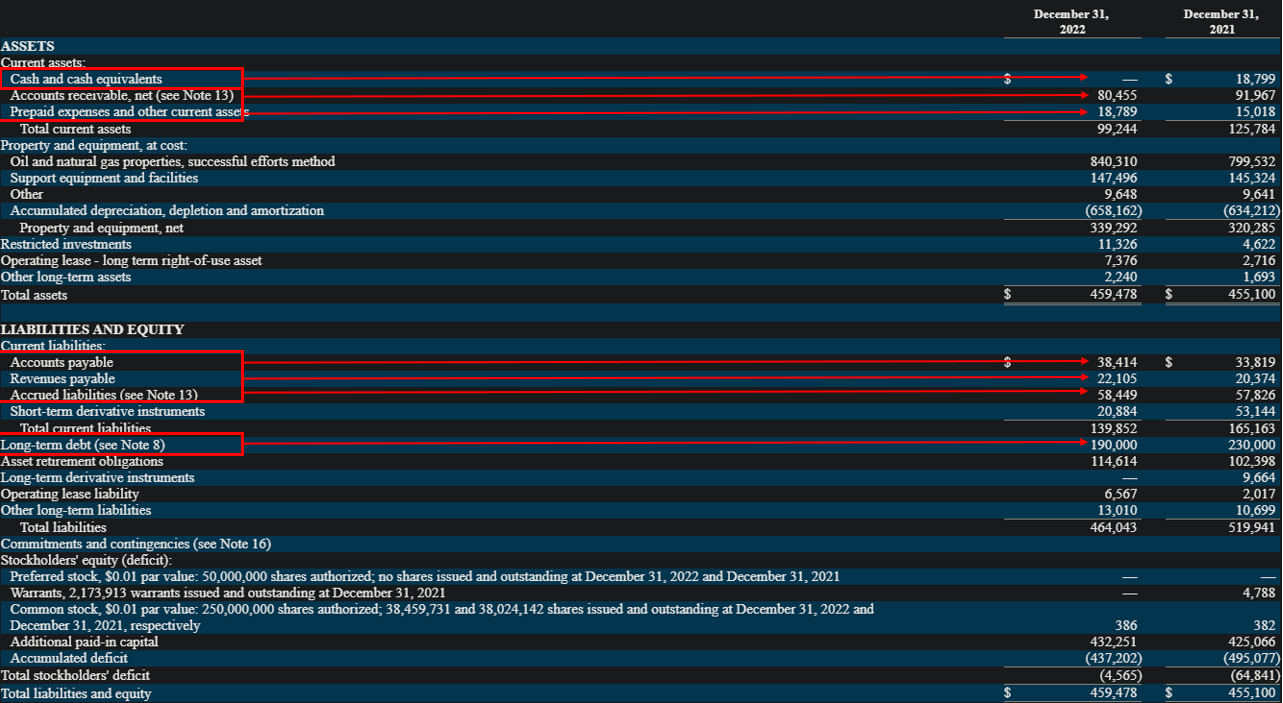

Taking Amplify Energy as an example, you begin with the net income of 57,875 million and add the tax expense of 111,000, the interest expense of 14,101 million, and the depreciation and amortization of 23,950 million. Following that, adjustments are made for non-recurring costs, such as the pipeline incident settlement cost of 12 million. Further adjustments could be considered, such as owner salaries or benefits. The Adjusted EBITDA for Amplify would then be 108,037 million.

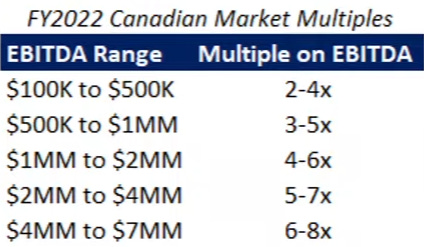

Now, the next step is to define the multiple to calculate the enterprise value. It's evident that the multiple will be at a premium the higher the EBITDA. It's worth noting that these tables can vary for different regions or sizes.

Fundamental Factors:

If the seller is selective about the buyer, a premium is likely on the multiple.

The sector outlook plays a crucial role; for example, the AI sector might command a higher multiple than a printing company.

Certain businesses like nightclubs or tobacco companies may struggle to secure financing, leading to a discount.

The buyer's preference for cash can result in a discount. Sellers might consider distributing risk, possibly through a vendor note.

A significant concentration with one customer or supplier poses a risk and may lead to a discount.

If the business heavily relies on the owner, a discount may apply. Assessing if the staff can effectively run the business is crucial.

Early departure of the seller or the potential exit of family members creates transition risks, impacting the multiple.

Declining gross margins or stagnant revenues may influence the multiple.

The ability to increase prices or charge a premium compared to the competition affects the multiple.

Factors such as ease of acquiring new customers, marketing costs, and customer retention play a role.

Customer dependence and high switching costs contribute to a higher multiple.

Premium margins, exceeding 20% EBITDA, positively impact the multiple.

Consistent revenue growth over several years enhances the multiple.

Businesses with low capital expenditures often command a higher multiple.

The availability of growth opportunities and room for expansion influences the multiple.

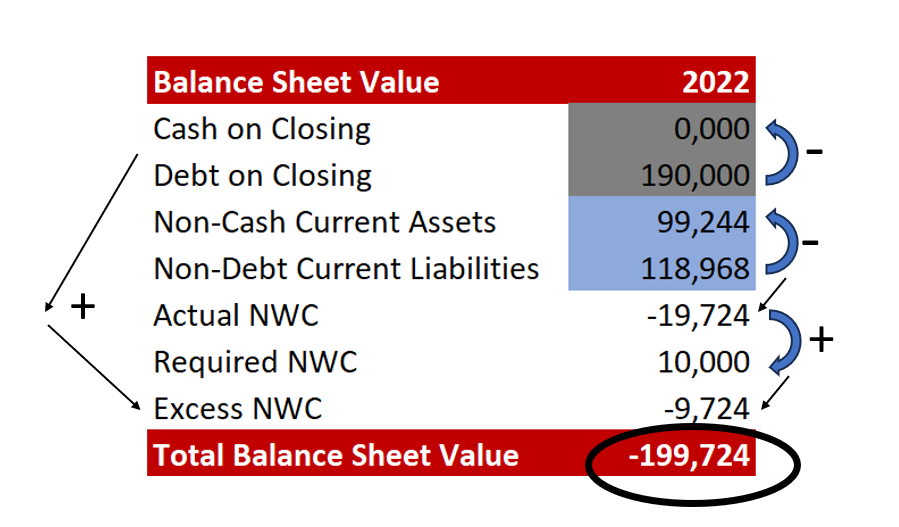

In addition to considering the Enterprise Value (EV), it is essential to incorporate the Excess Balance Sheet Value. Here is how you calculate it, using Amplify Energy as an example.

First, you take the cash and debt and subtract them. Similarly, you subtract the Non-Cash Current Assets and the Non-Debt Current Liabilities, resulting in the Actual Net Working Capital (NWC). The next step involves negotiating a required NWC, a topic I'll delve into in a future post. The formula for Excess NWC is Actual NWC minus Required NWC. Finally, you take the Excess NWC and add the difference between cash and debt to arrive at the Total Balance.

The formula for Private Company Value is given by:

Private Company Value=(108,037M×Multiple)+(−199,724)

I won't assume the multiple for Amplify at this time. In a future post, I plan to conduct a comprehensive case study on a privately held company.

Thanks,

Finn